Why in news?

MSCI's quarterly rebalancing of its global benchmark indices came into effect recently, triggering a sharp sell-off in Indian stock markets — with benchmark indices ending 1.5% down.

Foreign Portfolio Investors (FPIs) accounted for around 69% of the total NSE turnover of ₹2.87 lakh crore on the day of rebalancing — highlighting just how powerfully MSCI's decisions move Indian markets.

What’s in Today’s Article?

- What is MSCI and Why Does It Matter?

- What Changed in the Latest Rebalancing?

- The Taiwan Story — AI and Semiconductors

- India's Structural Weakness — No AI Play

- FPI Exodus from India — The Capital Flight Story

What is MSCI and Why Does It Matter?

- MSCI (Morgan Stanley Capital International) is a New York-based financial firm that creates and maintains global benchmark stock indices — essentially lists of companies from across the world, grouped by country and region, with specific weights assigned to each.

- These indices are keenly watched by investors worldwide because they directly dictate the flow of capital — particularly from passive funds (funds that simply mirror an index rather than actively picking stocks).

- When MSCI increases a country's weight, funds automatically buy more of that country's stocks.

- When the weight falls, they sell. This mechanical buying and selling can trigger massive market movements — as seen in India recently.

- MSCI Rebalancing

- Every quarter, MSCI reviews and adjusts its indices — adding or removing companies, and changing the weights assigned to countries based on factors like market capitalisation, share price performance, and liquidity.

- This is called rebalancing.

What Changed in the Latest Rebalancing?

- The number of Indian companies in the MSCI Global Standard index remained unchanged at 165 — but there were compositional changes (few companies removed and few others added).

- India's weight in MSCI Global Standard index — edged down from 12.4% to 12.3%.

- India's weight in MSCI Emerging Markets (EM) index — has been on a downward trend since peaking at around 21% in September 2024 and now stands at 11.94%.

- India vs Asian Peers — The AI Gap

- India's declining weight in the MSCI EM index tells a larger story about the structural shift in global equity markets driven by Artificial Intelligence (AI).

- Taiwan - 24.84%

- China - 23.05%

- South Korea - 18.69%

- India - 11.94%

The Taiwan Story — AI and Semiconductors

- Taiwan has surged ahead driven entirely by AI-driven demand for semiconductors. Taiwan Semiconductor Manufacturing Company (TSMC) — the world's largest chipmaker — has seen its share price more than double in the last year.

- TSMC is one of only two non-US entities in the world's top-10 most valuable companies — the other being Saudi Aramco.

- Taiwan recently overtook India to become the fifth most valuable stock market in the world by market capitalisation.

- MSCI described the catalyst bluntly — "AI. Specifically, the scale of AI-driven demand for semiconductors."

India's Structural Weakness — No AI Play

- The absence of a significant AI or semiconductor play in India's stock market — earlier viewed as a contrarian strategy — has now become a glaring structural weakness.

- India's top two companies by MSCI weight — HDFC Bank and Reliance Industries — each have a weight of only 0.79% in the EM index, compared to TSMC's 14.21% alone.

- As MSCI noted, "broad EM exposure today is structurally different than a year ago — with more technology, more semiconductors, and a more direct stake in the global AI build-out."

- India, with its IT sector dominated by services rather than semiconductor manufacturing, is structurally absent from this global AI wealth creation wave.

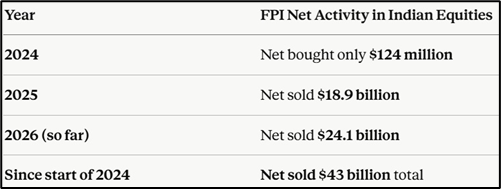

FPI Exodus from India — The Capital Flight Story

- The MSCI weight decline and India's AI gap are directly reflected in how Foreign Portfolio Investors have been treating Indian equities — with sustained and accelerating selling:

- This sustained FPI outflow — compounded by the rupee's depreciation making Indian assets less attractive in dollar terms — is creating a negative feedback loop: FPI selling weakens the rupee, a weaker rupee reduces India's dollar-denominated market cap, which reduces India's MSCI weight, which triggers more passive fund selling.