Context:

- India imports nearly 90% of its crude oil, making it acutely vulnerable to global price shocks, currency fluctuations, and geopolitical disruptions.

- Despite decades of reforms, the country's fuel pricing mechanism remains caught between market logic and political compulsion.

- This is a grey zone that breeds opacity, distorts incentives, and periodically destabilises public finances and oil marketing companies (OMCs) alike.

From APM to 'Managed Deregulation':

- Pre-2010 - The Administered Pricing Mechanism (APM):

- Before 2010, India operated under the APM, where the government directly fixed petrol and diesel prices — largely insulated from global crude markets.

- State-owned OMCs like Indian Oil Corporation (IOC), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL) sold fuel below cost, with losses compensated through:

- Direct subsidies

- Upstream support (from ONGC and Oil India)

- Oil bonds — deferred liabilities passed on to future governments

- While consumers benefited from stable prices, the system severely distorted price signals and strained government finances.

- The reform trajectory:

- 2010: Petrol deregulated, based on the Kirit Parikh Committee recommendations.

- 2014: Diesel deregulated.

- 2017: Daily price revision mechanism introduced.

- On paper, India embraced market-based pricing. In practice, it never truly let go.

The Grey Zone - What 'Managed Deregulation' Really Means:

- Structural asymmetry: Prices are nominally linked to global crude rates and the rupee-dollar exchange rate, but government tax policy decisively shapes the consumer outcome.

- Who benefits when crude prices fall?

- Central and state governments raise taxes silently.

- OMCs accumulate windfall profits.

- Consumers pay broadly unchanged pump prices.

- The numbers:

- Between 2022 and 2025, crude oil prices dropped from $99 to $68 per barrel, but combined tax collections of central and state governments from petrol and diesel increased from Rs 5.24 lakh crore to Rs 6.31 lakh crore.

- At the same time, oil marketing company profits surged — Rs 83,000 crore in 2024 and Rs 50,000 crore in 2025. However, consumers saw no benefit.

- Who bears the loss when crude prices rise?

- The current Strait of Hormuz crisis and broader geopolitical tensions are pushing crude prices higher.

- OMCs are now reporting losses of ~₹20/litre on petrol, and losses of up to ₹100/litre on diesel.

- Yet retail petrol in Delhi remains around ₹95/litre — held artificially low under political pressure.

- The system that quietly captured gains during the downcycle is now ill-equipped to absorb losses in the upcycle. An inevitable price hike looms.

Key Challenge - Structural Opacity and Asymmetric Risk:

- The core problem is the absence of a rule-based, transparent pricing architecture.

- This creates -

- Consumer mistrust: No visible logic behind pump prices.

- Fiscal distortion: Taxes used as a silent revenue lever rather than a policy instrument.

- OMC vulnerability: Companies forced to absorb losses that should be passed through.

- Investment uncertainty: No predictable margin framework discourages private sector participation.

- Macroeconomic risk: Sudden large price corrections are more destabilising than gradual adjustments.

Way Forward - The Fuel Price Transparency Framework (FPTF):

- The core architecture:

- The proposed FPTF would make every component of the pump price visible and rule-bound.

- For example, pump prices should be linked directly to oil prices, exchange rates, ethanol blending, refining and marketing costs, company margin and government taxes.

- Step-by-step calculation:

- If crude is at $100 per barrel and the exchange rate is Rs 93 per dollar, one barrel/ 159 litres costs Rs 9,300/ Rs 58.5 per litre.

- Petrol in India is blended with about 20% ethanol. With petrol at Rs 58.5 per litre and ethanol at Rs 60 per litre, the blended cost comes to around Rs 58.8 per litre.

- Add 15% to cover refining, transport, marketing, dealer commissions, and company margins, bringing the cost to roughly Rs 67.6 per litre.

- With combined central and state taxes currently around Rs 28.9 per litre, the final pump price comes to about Rs 96.5 per litre — very close to prevailing prices.

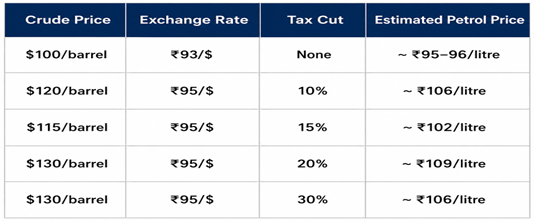

- Managing a price hike under FPTF: (Different scenarios)

- Key insight: The FPTF does not eliminate price increases — it makes them understandable, calibrated, and accountable. Tax cuts become a policy lever, not a political surprise.

India's 3-Pillar Energy Security Strategy:

- Adopt FPTF: A rule-based, formula-driven pricing system.

- Secure long-term crude contracts: Deepen supply partnerships with Russia and other reliable suppliers, independent of external geopolitical pressure. Supply diversification reduces vulnerability to single-source disruptions.

- Accelerate domestic exploration: Invest aggressively in India's sedimentary basins to reduce the 90% import dependence over the long term. This is as much a strategic imperative as an economic one.

Conclusion:

- India's fuel pricing story is one of reforms half-taken and accountability deferred.

- A FPTF is not merely a technical fix — it is a governance reform. It restores consumer trust, shields OMCs from politically-induced losses, gives governments a calibrated fiscal tool, and sends credible signals to investors in India's energy sector.

- For an economy that runs on imported oil, transparent pricing, diversified supply, and domestic exploration are not policy options — they are macroeconomic necessities.