Why in news?

Following the recent escalation of the West Asian conflict, India's economy has begun feeling the strain.

In just two weeks, foreign exchange reserves fell by $19 billion, the rupee weakened by 2.9% to ₹93.72, and stock markets dropped nearly 9%. Foreign investors have pulled out ₹1.03 lakh crore (~$11 billion) from India in March 2026 alone, reigniting concerns about external sector vulnerability.

What’s in Today’s Article?

- Foreign Exchange (Forex) Reserves

- India's Historical Vulnerability: From 1991 to the Present

- Current Concerns and the Road Ahead

Foreign Exchange (Forex) Reserves

- Forex reserves are funds held by a country's central bank in foreign currencies (like the US dollar). They act as a financial buffer during times of economic stress.

- Their key roles include:

- Funding the current account deficit (CAD) — the gap between what India earns and spends in foreign exchange.

- Smoothening rupee volatility by selling dollars when foreign investors pull money out (FPI outflows).

- Strengthening a country's overall macroeconomic credibility.

- Even if the CAD is small (currently ~1% of GDP), funding it becomes difficult when capital outflows are high — making adequate reserves critical.

- Where Do India's Forex Reserves Stand Today?

- As of March 13, 2026, India's forex reserves stood at $709.75 billion (RBI data).

- This is enough to cover over 12 months of imports, which is considered very comfortable.

- India is currently well above the danger zone, but the recent depletion warrants attention.

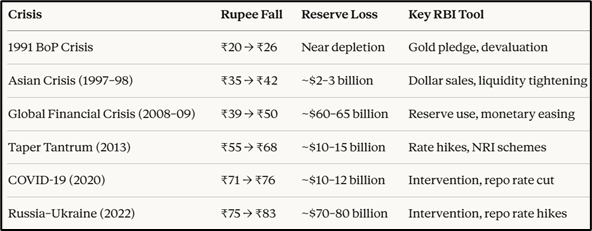

India's Historical Vulnerability: From 1991 to the Present

- India has faced external sector stress multiple times since independence.

- The most severe was the 1991 Balance of Payments (BoP) Crisis, when reserves fell so low that India could barely cover 2–3 weeks of imports — a near-bankruptcy situation that forced India to pledge gold and seek IMF assistance.

- Steps Taken to Address the 1991BoP Crisis

- Pledged 20 tonnes of gold with the Union Bank of Switzerland to raise $200 million

- Shipped 47 tonnes of gold to the Bank of England to raise $405 million

- Devalued the rupee in two tranches (9% and 10%) within three days — a total fall of ~18.7% against the dollar (₹20–21 → ₹25–26)

- The crisis forced the then government to launch landmark economic reforms — abolition of trade licences, rupee convertibility on current account, opening up to FDI, and capital market liberalisation.

- Since 1991, similar (though less severe) pressures have arisen during:

- Asian Financial Crisis (1997) - Regional currency contagion

- Global Financial Crisis (2008) - Capital flight from emerging markets

- Taper Tantrum (2013) - US Fed signaling rate hikes, FPI outflows

- COVID-19 Pandemic (2020) - Global uncertainty, rupee pressure

- Russia-Ukraine War (2022) - Crude oil shock, current account widening

- West Asian Conflict (2025–26) Ongoing — current episode

- Each crisis tested India's external sector differently, but the consistent lesson has been the importance of building and maintaining adequate forex reserves as a first line of defence.

Current Concerns and the Road Ahead

- Despite healthy reserve levels, several risks are building up:

- FPI Outflows — Foreign Portfolio Investors (FPIs) are pulling money out of Indian equity and debt markets, increasing demand for foreign currency and putting pressure on the rupee.

- Crude Oil Prices — India imports over 85% of its oil. A prolonged West Asian conflict could push oil prices higher, widening the trade deficit.

- Supply Chain Disruptions — Conflict-related disruptions could affect India's imports and exports, straining the Balance of Payments (BoP).

- Widening CAD — Higher oil import bills combined with capital outflows could push the Current Account Deficit higher, requiring more forex to fund it.

Conclusion

India's forex reserves are currently robust, but the West Asian conflict is a reminder that external shocks can erode buffers quickly. The RBI's ability to intervene in currency markets depends on maintaining adequate reserves.